New decarbonization ambitions discussed at IMO’s ISWG-14

The latest intersessional IMO meeting (ISWG-GHG 14 at London, 20-24 March 2023) provides important clues on what might be agreed in the revised GHG strategy in July 2023.

As stated by UMAS, since the IMO’s ISWG-GHG 14 conference outcome left up a wide range of possibilities for crucial components of the modification of the GHG reduction strategy but many of the specifics are still uncertain. The July MEPC 80 conference and the fifteenth Intersessional Working Group on Greenhouse Gases (ISWG GHG 15) will follow the fourteenth Intersessional Working Group on Greenhouse Gases (ISWG GHG 14), which is the penultimate working group meeting for the IMO’s GHG.

MEPC 80 will be a critical moment for the IMO because it coincides both with the adoption of a Revised GHG Reduction Strategy (Revised Strategy), as well as being the point that a set of policy measures key for enabling that strategy.

Whilst ISWG-GHG 14 was another point in the process of trying to achieve convergence, it was not a decision point on either strategy or policy measures, UMAS adds. The meeting can, however, provide some useful insights into how the debates might conclude at MEPC 80, although the details will remain in flux the final adoption.

| Read More: ICS Disappointed With Lack of Progress in Latest IMO Meeting |

The IMO has four critical and interrelated debates evolving in parallel, all due for MEPC 80 in July 2023:

- How will the lifecycle GHG emissions of international shipping’s energy use be calculated? (expected for finalization at MEPC 80, likely to receive further development this decade)

- What are the pathway/rates of GHG reduction that IMO will aim to achieve, and what overall strategy will guide IMO’s GHG reduction efforts? (expected for finalization at MEPC 80, unlikely to then receive any further modifications before 2028)

- What combination of policy options (e.g. carbon/GHG pricing, fuel standard etc), and what specifics of those policy options will regulate and incentivize the agreed rates of GHG reduction (expected to move into finalization phase at MEPC 80, may then finalize in the subsequent 1-2 years and enter into force within 2-4 years)

- Will the Revised Strategy represent a commitment to supporting a just and equitable transition to guide the further work on mid-term measures and other relevant initiatives effectively operationalize this, UMAS wonders

Area of focus

As reported by UMAS, particular attention has focused on levels of ambition, mid-term measures, the ‘basket’ or combination of measures to be finalized and revision to IMO’s Data Collection System (DCS). Progress was made in cleaning and clarifying non-contentious parts of the Revised Strategy, and refining some of the options that will be further debated and finalized in July.

The outcome text for this meeting, in combination with the preferences expressed during the week, provides clues as to what might be agreed at MEPC 80:

- The large majority of those who spoke (31/45) were clear that international shipping needed to reach zero GHG emissions by 2050 and that all of this GHG reduction would have to come from the international shipping sector – not from out of sector offsets, e.g. fundamental technology change is needed within international shipping.

- To help stimulate the uptake of new fuels, there was broad support for a fuel use target (5% by 2030), albeit with no agreement on the subset of fuels this would be applied to: low carbon/zero carbon/zero GHG/near-zero GHG

- A majority of countries wanted a 2040 GHG reduction target to be defined, at a magnitude of GHG reduction in line with the 1.5 degree temperature goal

- Nearly all countries who spoke want to see these reductions regulated by a technical element such as a fuel standard (e.g. limit on GHG emissions reducing over time), and an economic element (e.g. a carbon price), with these policy measures designed to support the transition. Most spoke to an objective of the economic element (e.g. a carbon price) being to support just and equitable transition (e.g. revenues deployed to increase equity), but there is significant ambiguity on what this means in practice.

Therefore, much of the specifics remains undecided as we head towards MEPC80 with only one intersessional meeting left (the week before MEPC 80) to bring the group to agreement on the levels of ambition/GHG targets, both magnitude of reductions, and scope (well-to-wake/tank-to-wake), the objectives and timing on the finalization and entry into force of mid-term measures, and the specifics of how just and equitable transition will be expressed in the strategy, and in the specification of the measures used to achieve the transition.

Levels of ambition

The initial strategy contains a 2030 and 2050 carbon intensity target, and a 2050 GHG target. The numerical values of these targets provide an indication of the expected rate of decarbonization of international shipping or the pathway. They provide the input to the stringency at which policy measures are designed, as well as a signal to industry of the rate of technology change that they can expect and need to set strategy for.

The revised strategy is considering strengthening of the existing targets, as well as adding additional targets. Prior to the meeting submissions were made from various Members on Levels of Ambition.

ICS expresses disappointment

The International Chamber of Shipping (ICS), announced they are disappointed with the levels of ambition discussed at the committee.

"We are disappointed by the lack of progress on setting new levels of ambition for GHG reductions to provide shipping with a clear net zero target for 2050. But we remain optimistic that a deal can still be stuck at the crucial MEPC meeting in July. More positively, governments are increasingly understanding the value of the ICS Fund and Reward proposal to accelerate the production and uptake of low and zero-carbon fuels", said Guy Platten, the Secretary General of the International Chamber of Shipping.

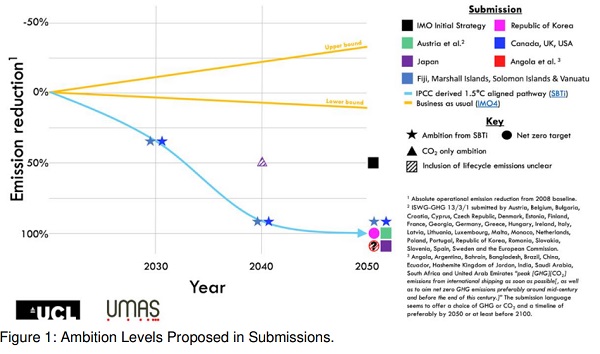

Ambition Levels Proposed in Submissions

Going into the meeting, submissions showed that both a group of developed economies (UK, US, Canada), and separately a group from the Pacific (Fiji, Marshall Islands, Solomon Islands, Vanuatu) had endorsed the GHG reductions of the Science Based Targets Initiative’s 1.5- aligned pathway.

This pathway is derived from the IPCC’s reports, so helps to provide a climate-science derived quantification of ambition that signals clear alignment to the 1.5 temperature goal of the Paris agreement. Other countries had done their own analyses and proposed different numbers. Notably, the addition that has gained the greatest support this meeting is for a 2040 target.

The IMO is preparing a fuel/technology availability study which will provide information to the next negotiation on the viability of these reduction levels and their different pathways. From a side-event presentation of preliminary results, targets with deep GHG reductions in 2040 and 2050 appear viable, but the highest level of 2030 reduction (54% reduction on 2008) did not.

2030 Level of Ambition targets

Around 37 members signaled preference, in either submissions or interventions, to include an absolute reduction target for 2030 in this Revised Strategy with proposals varying between giving a percentage or simply a placeholder for now. Of the speakers at the meeting, approximately an even number of countries supported a strengthened target, taken from SBTi, to the countries that supported leaving the target as it currently exists. Those member states that preferred to leave the 2030 intensity target without an accompanying absolute target pointed to the short period of time until 2030 and the challenge of any significant change at this point, as well as the risks of adverse impacts. Many also mentioned the review of short-term measures (EEXI and CII) which is due by 2026, as a source of insights that would be needed before any revision.

- Strengthening (37% GHG reduction relative to 2008)

- No change to initial strategy (no absolute target, only at least 40% reduction in carbon intensity relative to 2008)

The drafting that will progress to ISWG-GHG 15 uses both of these as two options for further consideration, in addition, they are also both represented as CO2/GHG intensity (40%/65%) reductions relative to 2008. This implies that these values represent the range of likely outcomes e.g. that a third value between the two may ultimately be selected.

There was also further discussion of a potential uptake target for use of new fuels by 2030. The concept behind this target was to specify a minimum amount of early adoption of new fuel that could constitute a tipping point, allowing subsequent rapid scaling and further use in the 2030’s. This concept was broadly supported by countries in a range of circumstances both at previous meetings, and also at this meeting.

| Read More: IMO Secretary-General updated on Black Sea Grain initiative |

There are however two difference preferences:

- The language used to define fuels that this target is applied to. For example, some prefer “low/zero carbon”, others prefer “zero/near-zero GHG fuels”. Both are included as options for now. Low/zero carbon risks legitimizing cleaner fossil fuel (e.g. LNG), or grey hydrogen derived fuels as contributing towards the target, which would then undermine investments into more expensive fuels that are expected to be required in the long-run and defeat the objective of this target, as it was originally conceived.

- The language used to define how the 5% is accounted (mass or energy). Fuels are not equivalent in energy density, so these result in differences depending on which is ultimately chosen.

Among the interventions and indeed the side events it was clear that alongside first movers, energy efficiency technologies are key for reducing emissions this decade and thereafter, as the fuels transition scales up, are key for reducing fuel costs for the less energy dense new zero emission fuels.

2040 Level of Ambition

2040 represents an additional milestone in the pathway, or, as it has also been referred to a checkpoint for ‘ensuring progress’, and for phasing out emissions. Between submissions and speakers during the meeting the support for a 2040 ambition being added to this Revised Strategy was around 43 Member States and whilst all countries speaking at the meeting could support the concept of a 2040 ambition, a minority thought it should only be defined in the future i.e. during the next revised strategy which would be adopted in 2028.

The largest group of countries who spoke at this meeting proposed a 96% reduction in GHG (aligning with the SBTi pathway), and a small number thought 50% reduction in GHG was more appropriate.

A large group of countries spoke to there needing to be a ‘1.5-aligned’ 2040 ambition, but were not specific about what the value should be. A range of values bounded by 50% and 96% are included in the drafting that will go to further consideration at ISWG-GHG 15.

- Added at 96%

- Added at 50%

- 1.5 aligned ambition/checkpoint

- Defined in the future

Notably, within the 7 speakers that support a 1.5 aligned ambition/checkpoint in the 2023 Revised Strategy are some speakers from a large group who normally coordinate their position – indicating the level of support for ‘1.5-aligned’ could be very substantial. Additionally four professional and industry associations supported the addition of a 2040 target and no industry members spoke to favor postponement to the following revised strategy in 2028.

2050 Level of Ambition

Outside of the IMO, most of the discussion and focus has been on the 2050 target, so this is perhaps the most symbolically important, even if it is also the target that is furthest in the distance and therefore the least likely to have near-term impact on the sector. This may be because the wider discourse around UNFCCC COP and national ambitions often uses “net zero by 2050” as a guiding intent, and many companies have expressed their alignment to such targets.

In both submissions and interventions around 45 member states support a zero or phase out of emissions by no later than 2050. The main differences of opinion are between those who favor ‘no later than 2050’ and those favoring a vaguer ‘aim [for] net zero GHG emissions preferably around mid-century and before the end of this century.‘ While this may appear to be an issue of language only, the vague working could leave the point that emissions can reach zero up to around a decade or more later. A couple of members noted the tension between a 2050 date for the international sector being in conflict with their own national targets for 2060.

Another difference is in the definition of ‘zero’: whether it implies full GHG reduction from within shipping, or the legitimizing of offsetting GHG emissions in international shipping using credits of emission reductions from outside international shipping (which net zero implies). Of the speakers at the meeting the split on ambition fell as follows:

- Zero or phase out emissions by no later than 2050

- Net zero by 2050 but clear on no out of sector offsets

- Net zero by 2050 but not clear about no out of sector offsets

- Net zero around mid-century

The speakers on zero or phase out of emissions by no later than 2050 included some members of a larger group of countries who normally coordinate. So while 29 Members spoke, this number likely represents a greater number of countries. The large majority who spoke supported the highest ambition definition with these parameters – zero GHG on a well-to-wake basis no later than 2050.

Well-to-wake or tank-to-wake, CO2 or GHG?

Previous rounds of debate have seen a divergence of opinion on whether the IMO’s targets/ambitions should be defined as well-to-wake, tank-to-wake, CO2 or GHG emissions.

Similar differences in opinion occurred at this meeting. Generally, GHG framing is gaining greater support and appearing increasingly in preference to CO2 framing.

However, the term carbon intensity is still being considered for use in the context of the 2030 ambition. Instead of defining tank-to-wake or well-to-wake at the level of individual targets (2030, 2040, 2050), the draft text that will be negotiated further uses an overarching statement that to some extent all ambitions will be applied within a well-to-wake framing.

| Read More: IMO, Norway and Singapore sign MoU on maritime decarbonization |

However, there were differences between member states, and so this will need to be further discussed at the next meeting. This item’s definition is also likely to be related to the LCA guidelines which are under development in a parallel process, so along with the development of measures, will be clearest when more specifics have been finalized – hopefully at MEPC 80.

Concerns remain those expressed in earlier rounds of debate and discussed in greater detail in earlier readouts.

"This meeting marked a growing clarity on likely ambition for 2050 and also 2040, which is a positive sign for an equitable transition which, at its core, requires targets aligned with limiting temperature rise to 1.5 or below. However, despite the repeated support across meetings for a just and equitable transition that leaves none behind – there is little sign of this commitment being embedded throughout the revised strategy as of yet", said Dr Aly Shaw, Policy Lead at UMAS

"It is hard to overstate how important the MEPC 80 outcomes will be both for society’s efforts to avoid dangerous climate change, but also for the shipping sector. Reading from the numbers of how many support high ambition outcomes, there are positive signs. But this is a simplistic way to estimate how these debates will conclude. The nature of the off-IMO debate leading up to MEPC 80 is therefore crucial", said Dr. Tristan Smith, Director of UMAS

Source: Safety4sea

| Read Here | |

|

|